ULIP vs Mutual Funds: Which Is Better for Your Portfolio in 2026?

If you've been approached by an insurance agent offering a "wealth-building" ULIP (Unit Linked Insurance Plan), or you're confused about whether to invest in ULIPs or mutual funds, you're not alone. This is one of the most common questions I receive from clients across India.

Table of Contents

ToggleThe short answer? For most investors, mutual funds are the better choice. But let's dive deeper to understand why—and when a ULIP might actually make sense.

What Are ULIPs vs Mutual Funds?

ULIPs (Unit Linked Insurance Plans)

A ULIP is a hybrid product that combines life insurance with investment. Here's how it works:

- You pay a premium (e.g., ₹50,000/year)

- Part of it goes toward life insurance coverage

- The remaining amount is invested in equity, debt, or balanced funds

- You get both a death benefit (insurance) and potential wealth growth

The catch? ULIPs are heavily structured with a 5-year lock-in period and hefty charges.

Mutual Funds

A mutual fund pools money from multiple investors and invests in stocks, bonds, or a mix of both. You own "units" representing your share of the portfolio. Key features:

- Complete flexibility—exit anytime (with tax implications)

- Lower expense ratios (typically 0.5–1.5% for equity funds)

- No lock-in periods

- Transparent, daily Net Asset Value (NAV) pricing

Head-to-Head Comparison

| Feature | ULIP | Mutual Fund |

|---|---|---|

| Total Annual Charges* | 2.5–3% for first 10 years (fund mgmt + admin + mortality) | 0.5–1.5% per year (expense ratio only) |

| Lock-in Period | Mandatory 5 years | None (flexible exit) |

| Insurance Coverage | Automatic death benefit | None (separate term insurance needed) |

| Transparency | NAV updated monthly (opaque charges) | NAV updated daily (clear fee breakdown) |

| Tax on Gains (>12 months holding) | 12.5% LTCG (for policies after Feb 2021 with premium >₹2.5L/year; effective April 2026). Below ₹2.5L: May be tax-free if conditions met under Section 10(10D) | 12.5% LTCG (equity), 20% LTCG (debt) with ₹1.25L annual exemption |

| Surrender Charges | 0–3% in early years (heavy) | None |

| Fund Switching | Limited (3–4 free switches) | Unlimited (often free within same house) |

| Performance | Underperformance due to high costs | Better long-term returns (lower costs) |

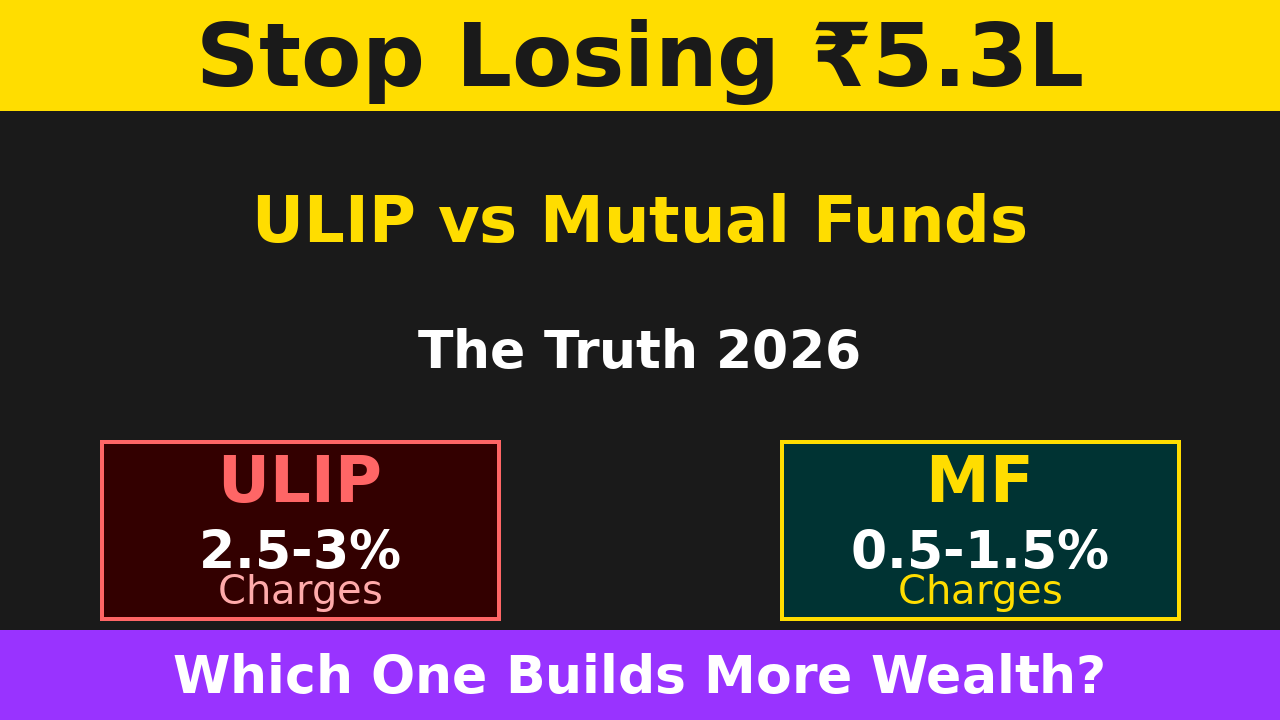

The Cost Impact: A Real Example (with 2026 Tax Rules)

Let's compare what happens with ₹50,000 invested annually for 10 years at 12% annual returns:

Gross corpus at 10 years: ₹87,55,000

Less: Tax on gains >₹1.25L per year: ~₹9,50,000

Final corpus: ₹78,05,000

Mutual Fund (1% annual expense ratio, 12.5% LTCG tax after April 2026):

Gross corpus at 10 years: ₹91,55,000

Less: Tax on gains >₹1.25L per year: ~₹8,20,000

Final corpus: ₹83,35,000

Difference: ₹5,30,000 more in mutual funds (6.3% better outcome!)

This difference compounds over 20–30 years into life-changing wealth. The average person misses ₹15–20 lakhs by choosing a ULIP over a simple SIP + term insurance combination.

What Are ULIP Charges Broken Down? (2026 Rates)

ULIPs don't have one "expense ratio"—they have multiple overlapping charges:

- Premium Allocation Charge: 2–10% of your first premium (agent commission hidden here)

- Fund Management Charge (FMC): Capped at 1.35% per year by IRDAI (deducted daily)

- Policy Administration Charge: ~₹50–500/month or up to 2.25% per year (fixed cost)

- Mortality Charge: Cost of life insurance, varies by age and sum assured

- Surrender Charges: Up to 0.5% per annum if you exit early (first 5 years)

- GST on Charges: As of Sept 2025, GST reduced to 0% on life insurance premiums (good news!)

Total impact: IRDAI caps total charges at 3% for the first 10 years and 2.25% thereafter. But this still exceeds most mutual fund expense ratios (0.5–1.5%).

When MIGHT a ULIP Be Suitable?

ULIPs aren't useless—they're just overpriced for most investors. Consider one only if:

- You have no term insurance and absolutely cannot buy it separately (though this is rare and unwise)

- You need forced savings discipline and cannot stick to a voluntary SIP

- You have very specific regulatory/inheritance needs (rare for individual investors)

Even then, the proper approach is to buy term insurance separately (~₹2,000–5,000/year for ₹1 crore coverage) and invest the rest in low-cost mutual funds. You'll come out 5–10 years ahead.

The Better Strategy: Term Insurance + Mutual Funds

The Math (₹50,000/year budget):

Option 1 (ULIP):

₹50,000/year → ₹3,500 insurance + ₹46,500 invested (with 3% drag) = ₹8.6L after 10 years

Option 2 (Term + MF):

₹2,500/year → Term insurance (₹1 crore coverage)

₹47,500/year → Mutual funds (1% costs) = ₹11.4L after 10 years

You get: Same insurance + 25% more wealth + Full flexibility

Tax Implications: ULIP Changes in 2026

Until 2025, ULIP taxation was murky. But Budget 2025 brought clarity: high-premium ULIPs (annual premium >₹2.5 lakh) now face LTCG tax at 12.5% effective April 1, 2026. Here's the breakdown:

If annual premium ≤ ₹2.5 lakh:

Maturity proceeds: Tax-free under Section 10(10D) (if premium < 10% of sum assured)

If annual premium > ₹2.5 lakh:

Gains taxed as LTCG at 12.5% (held >12 months)

Short-term gains taxed at 20% (held ≤12 months)

Equity Mutual Funds (for comparison):

LTCG: 12.5% on gains >₹1.25L (held >12 months)

Gains up to ₹1.25L: Tax-free per financial year

The key difference now: ULIPs with high premiums and mutual funds are taxed similarly at 12.5%, but ULIPs still offer tax-free fund switching within the policy, while each mutual fund switch triggers a taxable event. However, this switching advantage doesn't offset the higher charges.

What About Your Existing ULIPs? (2026 Guidance)

If you already own ULIPs from ICICI Prudential, Bajaj Allianz, TATA AIA, or others, here's what to do based on your premium amount:

- Premium ≤ ₹2.5 lakh/year: These remain tax-efficient (tax-free maturity if conditions met). Keep if you also need the life cover. Otherwise, switch to mutual funds after 5 years.

- Premium > ₹2.5 lakh/year (issued after Feb 1, 2021): From April 2026, gains are taxed at 12.5% LTCG, same as mutual funds. These have zero tax advantage. Exit at maturity and move to mutual funds + separate term insurance.

- Don't exit in the first 3 years: Surrender charges and premium allocation charges will hurt badly.

- After 5 years: Lock-in period ends. Strongly consider withdrawing your corpus and moving to mutual funds.

- At maturity: Don't reinvest the lump sum back into another ULIP. Use mutual funds instead, paired with fresh term insurance.

Need Help Transitioning from ULIPs?

We offer a free portfolio review for HNI clients with multiple insurance products and outdated investments. Let's build a tax-efficient, low-cost plan together.

Get Free ReviewRecommended Mutual Funds to Replace ULIPs

If you're moving away from ULIPs, here's a simple framework:

- For equity allocation: HDFC Flexi Cap / ICICI Prudential Focused Equity (proven long-term performers)

- For debt allocation: HDFC Banking & PSU Debt Fund (lower volatility, better yields)

- For SWP strategy: Hybrid funds like HDFC Hybrid Equity or SBI Magnum Balanced Fund (steady income with growth)

- For systematic withdrawals: Pair with liquid funds for STP (Systematic Transfer Plan) to minimize exit timings

Check our detailed India Value Investing Deep Value Stock Report for hand-picked quality companies if you want a stock-picking alternative to mutual funds.

FAQ Section

No. Always compare post-cost, post-tax returns. A ULIP showing 12% gross returns may deliver 7% net (after 3% expenses + 35% tax). A mutual fund at 12% may deliver 10.2% net (after 1% expense + 10% tax). The gap compounds.

ULIP coverage is typically low relative to premiums (often 125–150% of annual premium as death benefit). If you have dependents, you need *real* term insurance (₹1 crore+). Don't rely on ULIP alone.

Don't exit (surrender charges are punitive). Continue paying premiums. Plan your exit at the 5-year mark. After 5 years, the fund is genuinely yours with no penalty.

Stick to your original allocation (don't panic-shift to debt). If anything, you have a few free switches per year—use them strategically, not reactively. Better yet, don't move to ULIPs in the first place.

Yes, but redirect it to mutual funds for better flexibility and lower tax treatment. We offer an SWP calculator to help plan systematic withdrawals efficiently.

The Bottom Line

ULIPs are financial products engineered to benefit insurance companies and their agents, not you. They combine high costs, poor tax treatment, and lack of flexibility into a single overpriced wrapper.

For 95% of Indian investors:

- Buy a separate term insurance plan: ₹500/month for ₹1 crore coverage

- Invest the rest in low-cost mutual funds: SIP of ₹25,000/month or lump sum in HDFC/ICICI flexi cap

- Plan your withdrawals intelligently: Use an SWP after 5+ years for tax-efficient income

This approach will leave you ₹20–30 lakh wealthier over a 20-year horizon. That's not a small difference.

If you're already stuck in a ULIP, don't panic—but start planning your exit at the 5-year mark. And if an agent calls offering a "special ULIP promotion," do yourself a favor: hang up and call your financial advisor instead.

- Take our free portfolio review if you're unsure about your current investments

- Use our term insurance + SIP calculator to see the real-world impact

- Subscribe to our Telegram channel for weekly financial tips and market insights

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Always consult with a registered financial advisor before making investment decisions. Past performance is not indicative of future returns. Mutual funds and stocks are subject to market risk—read the offer document before investing.